It's the economy stoopid

The Empire has no clothes!

a worldwide coup has been underway for centuries.

The invasions, coups, secret wars all have the aim of replacing

a countries economic infrastructure with a centralised Global bank.

|

The world financial system - two sides of the same coin-

addiction to a system? - Money dictated by belief...

Ted Nace's Gangs of America: The Rise of Corporate Power and the Disabling of Democracy charts the insidious, century-long accumulation of precedents constructed around a glaring judicial error, arising from the 1886 Santa Clara County v. Southern Pacific Railroad case, that has ultimately resulted in the extension of "equal protection" under the law to corporations, and the bestowal of "civil rights" and "immortal personhood" on economic entities, including the First and other Bill of Rights amendments intended to protect human individuals. This lethal absurdity has now become extraterritorial, as GATT and WTO measures enable corporations to file suit against sovereign states whose labor or environmental laws inhibit corporate profit-taking.

Disorganized Conspiracy

"The economic crisis for the general population is a global one. In the past 20 years, economic growth has fallen well below the levels of the 1950s and 1960s (which were, to be sure, historically unique). World per capita income fell in 1993 for the fourth straight year, while the unemployment situation, already grim, worsened in most countries. The International Labor Organization (ILO), in its World Employment 1995 report, "Predicts Rising Global Joblessness," the Wall Street Journal reports, noting however that "many management theorists" regard the analysis as outdated because "the whole concept of a job -- steady work at steady pay from the same employer -- must be discarded." The only major exception to the growing catastrophe of global capitalism is East and Southeast Asia, with the exception of the Philippines -- incidentally, the sole part of the fastest growing economic region of the world that has been under tight U.S. control for a century and (coincidentally) resembles the Latin American disaster area. "

Rollback - Part IV

by Noam Chomsky

"In 1919, Hitler was an Intelligence Officer with the German Army assigned to spy on the tiny German Labor Party. He became its leader. Max Warburg, brother of Paul Warburg, founder of the US Federal Reserve, was the chief of German Intelligence. Both were executives of the I.G. Farben conglomerate. There is no record of when Hitler stopped working for these Illuminati figures. "

Bankers Backed Nazism And Zionism

|

|

The following lifted from this source

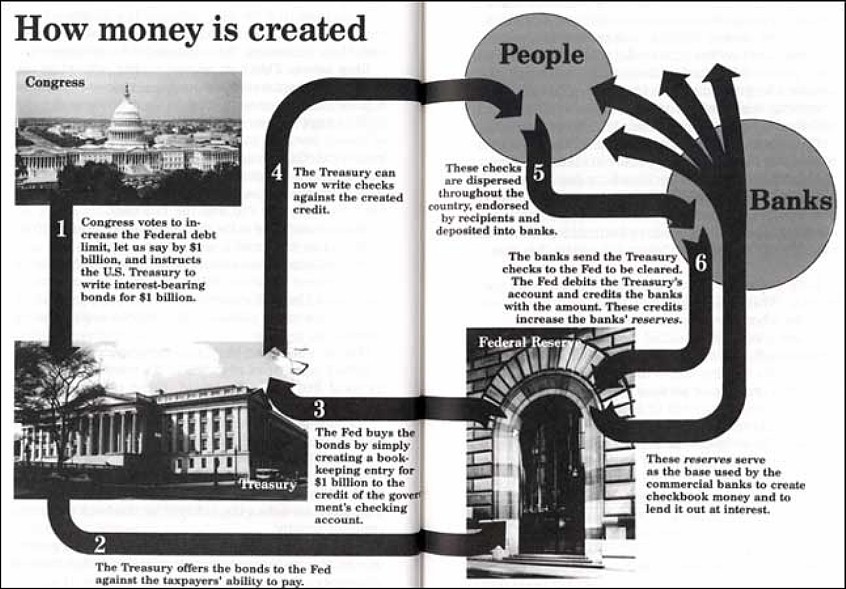

The financial system currently adopted by all nations is often

described as "debt based", since the process

of going into debt is relied upon almost exclusively to create

and supply money to their economies. By the action of

lending to borrowers, commercial banks create

credit and advance this to industry, consumers and governments.

This "bank credit" circulates in the broader economy until such

time as the loan is repaid. Such "bank credit" now forms 96% of

the money stock in most industrial nations, with a mere 4% the

notes and coins created by government, and free from a parallel

debt.

Thus, almost the entire money stock

is supported in circulation by vast debts in four

main sectors....

- Private debts eg. mortgages, loans, overdrafts, credit-purchases

- Industrial and commercial debts

- Government "national" debts

- International, including Third World debt

The supply of money is a direct product of borrowing, and debt

maintains this money in circulation. Modern debt is, in

aggregate, quite unrepayable. Furthermore,

difficulty is experienced in the repayment of individual debts

in all four sectors.

The Drive Behind Globalisation, 1998, pp 3-4.

Money is created in each of these four areas....

How BANKS CREATE MONEY for PRIVATE & COMMERCIAL Needs

If a bank makes a loan, nothing is lent, for the simple reason

that there is nothing of substance to lend. The bank makes what

it terms a loan against the amount of money deposited with it at

that time. This is all done with the utmost ease. The bank has

simply to agree that a person may take out a loan of, say,

£5,000. The person taking out the loan can then spend £5,000 and

hey presto! £5,000 of new number-money has been created. No one

with a bank account is sent a letter telling them that the money

in their account is temporarily unavailable, because it has been

lent to someone else. None of the original accounts in the bank

has been touched, reduced or affected. Nobody else's spending

power has been reduced, but £5,000 of new spending power has

been created; £5,000 of new number-money enters the economy at

the stroke of a bank managers pen, but £5,000 of debt has also

been created.

Thus, whoever takes out the loan will then make purchases and

payments to other people, who will pay that new money into their

bank accounts. Result: more bank deposits! As soon as the loan

in the example above is spent, £5,000 will find its way into the

bank account of a car dealer or DIY store; £5,000 of apparently

new money. This is money which has supposedly been loaned but

the banking system doesn't distinguish this fact. It simply

registers a new deposit, and regards it as new money. Total

deposits in the banking system have therefore increased by

£5,000. This is the boomerang effect of a bank loan by which a

loan rapidly creates an equivalent amount of new bank deposits

in the banking system. This effect was neatly summarised in a

statement by Graham Towers, former Governor of the Central Bank

of Canada....

"Each and every time a bank makes a loan, new bank

credit is created -- new deposits -- brand new money."

The new money will provide the banking system with the

collateral for more lending. This is the bolstering effect of a

bank loan. As the total money held by banks and building

societies becomes swollen by loans returning as new deposits

this provides them with the basis for further loans.

Perhaps the best description of this process of money

creation was provided by H.D. Macleod

:

"When it is

said that a great London joint stock bank has perhaps

£50,000,000 of deposits, it is almost universally believed that

it has £50,000,000 of actual money to lend out as it is

erroneously called... It is a complete and utter delusion.

These deposits are not deposits in cash at all, they are nothing

but an enormous superstructure of credit."

The Grip of Death, Jon Carpenter Publishing, 1998, pp. 11-13.

How BANKS CREATE MONEY for NATIONAL Needs

A country's national debt is completely separate from, and

additional to, the level of private and commercial debt directly

associated with the money supply. The United Kingdom

national debt in 1998 stands at approximately £380 billion. If

the private and commercial debt of £780 billion and the national

debt are added together, the total indebtedness associated with

the UK financial system stands at some £1160 billion, which

dwarfs the total money stock of £640 billion! How did this

condition of overall negative equity come about?

This excessive indebtedness -- which is a blatant

misrepresentation of the real state of economic wealth enjoyed

by the nation -- is a position shared by all the developed

nations.

The national debt is actually composed of thousands of pieces of

paper called stocks, bonds and treasury bills. These

stocks and bills, known as gilt-edged securities,

or gilts, are essentially elaborate forms of government IOU.

These IOUs are issued because each year the government

fails to collect enough in taxes to cover the costs of its

public services and other spending -- and it borrows money

to cover this shortfall. All government budgets overshoot by

many billions of pounds, dollars or deutschmarks annually. This

leads to what is called the borrowing requirement

for that budget year. A country's national debt is

therefore the total still outstanding on all past years'

borrowing requirements; thus the UK national debt

consists of £380 billion of these gilt edged IOUs, in the form

of outstanding treasury bills and stocks.

The method of issuing these IOUs and administering the national

debt is quite simple. In order to obtain money to cover its

annual spending shortfall, an appropriate number of government

stocks and bills are drawn up by the Treasury. These are then

sold in fact they are auctioned off in the money markets to the

highest bidder. This is done throughout the year to meet the

shortage of revenue as it arises, and the announcements, in the

form of government advertisements, can be seen regularly in the

financial press. These stocks and bills are bought because they

promise to repay a larger sum of money at some future date, and

are sold at a price that promises a good return to whoever buys

them. They are usually denominated in considerable sums of

£1,000 or more per bond and are bought by insurance

companies, pension funds, banks and trust funds... anywhere that

money accumulates as savings. By selling these stocks,

the government obtains the additional money it needs for the

public sector, making up the annual shortfall in what it can

gather by taxation.

As these government stocks mature and become due for payment,

the government has to find the money promised on those stocks,

and pay it to the financial institutions that bought them. But

governments are unable to pay this money owing on their past

stock issues. Indeed, each government is confronted by the

current year's annual shortfall in taxation

receipts. The whole reason for the government issuing

stock in the first place was because it could not cover its

expenditure through taxation, and this annual shortfall

is constant. There is no way a government can pay the money it

owes. How then can the government pay up on its maturing stock?

It has underwritten promises it cannot keep. What happens is

that the government obtains the money to meet the payments due

on maturing national debt stocks by selling more

government stock to the financial institutions --

promising even more money in the future. The government draws up

enough new stock to cover the repayments due on the old stock,

sells this, and uses the money to pay off the old stock. Of

course, when this new stock matures it too has to be paid off

from the sale of yet more stock. The government manages to pay

off the national debt, and not pay it, at one and the same time...

There is a pretence that this is not the true arrangement, since

repayment of national debt stocks is actually accounted as

coming from taxation, not from the sale of more bonds. But this

repayment from taxation creates such a massive shortage in

government revenues that can only be made up by the sale of more

bonds so the net effect is that repayment is constantly deferred

by the sale of further government bonds. This is what is

referred to as interest on the national debt although it is not

really interest in the conventional banking sense, but a

constant rescheduling of a completely un-repayable debt.

This deferral is not, however, the end of the story....

At the same time as deferring and re-mortgaging the

existing level of national debt, the government

has to sell yet more stock to cover the amount

by which taxation falls below what is needed to support its

public services. The national debt therefore escalates,

increasing by the amount required to re-mortgage the past

national debt, plus the shortfall in revenues to fund the public

sector. In 1960, the UK national debt was £26 billion; by

1980 it had risen to £90 billion. The national debt in 1998

stands at nearly £380 billion, and is likely to reach a trillion

pounds within the next 20-25 years. In America, the national

debt in 1960 stood at $240 billion; by 1997 it had reached the

level of $5,000 billion, or $5 trillion!

It should also be remembered that the money held by pension

funds and insurance companies, or whoever buys the government

stocks, is money that had to be borrowed into existence

in the first place. In other words, by this process,

governments borrow money which has already been borrowed into

existence, and they thus create a second massive institutional

debt in respect of money which already has a debt behind it!

Adding the national debt to the total of private debt places a

country and its people in a position of overall negative equity,

owing far more on paper than the amount of money that exists in

the economy.

The Grip of Death, pp. 96-98.

So, in summary: Governments draw up official treasury bonds, and

these are auctioned on the money markets. The bonds are bought

by both the banking and non-banking sectors. When the

non-banking sector (pension and insurance funds etc) purchases

the bonds, saved monies are recycled into the economy through

government spending. When the banking sector buys government

bonds, banks and lending institutions create credit: There is an

increase in the money stock. This money is spent into the

economy through government spending.

Creative Accountancy, 1998, p. 29.

How COINS and NOTES are CREATED

The significant point about coins and notes money created by the

government is that this money is created debt-free,

and spent into the economy by the government. This

is a vital consideration, and it is therefore important to

appreciate precisely how this injection of debt-free

money is managed. Coins and notes are minted and printed

by the government at no cost, apart from that of materials. Of

course, governments have no particular need of these coins and

notes; banks are the institutions requiring a supply of cash.

The government therefore sells the coins and notes that it

creates to banks, who pay by cheque, and the government acquires

the face value of those coins and notes in number-money. The sum

of money which the government obtains, and which is debt-free so

far as the government is concerned, is then added to whatever

taxation revenue has been raised to fund the public sector.

Thus, coins and notes are created by the government, and an

amount equivalent to the face value of those coins and notes is

spent into the economy as a direct, debt-free

input.

The Grip of Death, p. 14.

How INTERNATIONAL or Third-World DEBT is CREATED

The financial position of even the wealthiest nations is one of

acute financial pressure, with massive private and

national debt, and budgetary difficulty dominating the

economy. How can the wealthy nations, from a position of such

perpetual monetary shortage and insolvency, lend money to the

developing nations? The answer is that they do not. The

money advanced to Third World nations is not money loaned from

the wealthy nations. These sums consist almost entirely of

monies that have been created, via the commercial banking

mechanism, specifically for the purpose of the loan

concerned. In other words, the same debt-based, banking

process used to supply money to national economies is also

employed for the creation and supply of funds to debtor nations.

Thus, these monies are not owed by debtor countries to the

developed nations, but to private, commercial banks.

The WORLD BANK

Holding only a nominal reserve contributed by the wealthy

members, the World Bank raises large quantities of money by

drawing up bonds and selling these to commercial banks on the

money markets of the world. Thus, the World Bank does not

itself create the money it advances to Third World nations, but

sells bonds to commercial banks which, in purchasing these

bonds, create money for the purpose. The World Bank

therefore functions along the lines of a country's national debt.

Just as with the government bonds of a country's national debt,

when a commercial bank makes a purchase of World Bank

money-bonds, the commercial bank creates additional bank credit.

In essence, the World Bank acts as broker for commercial

banks, who are the actual money-creation agents and who hold

World Bank bonds in lieu of monies they create in

parallel with debts registered against Third World nations.

Although these loans may be denominated in pounds, dollars or

Francs, such loans advanced under the World Bank have no

connection with respective national economies, and in no sense

represent monies loaned by these nations, nor debts owed to them

by developing nations. The debts are owed to private,

commercial banks (via the World Bank) in respect of money they

have created through the purchase of debt bonds.

The INTERNATIONAL MONETARY FUND

The IMF presents itself as a financial pool an international

reserve of money, built up with contributions, known as quotas,

from subscribing nations -- that is, most nations of the world.

However, credit creation accompanies almost every aspect of IMF

funding....

Twenty-five percent of each nation's IMF quota is paid in the

form of gold, the remainder in the nations own currency. The 25%

gold quota is the only component of IMF lending capacity that

does not, in some way, constitute additional money created in

parallel with debt.

The 75% of a nation's quota payable in national currency is

invariably funded by the government concerned through the sale

of bonds, thus adding to that nation's national debt. Therefore

the IMF, whilst not itself creating credit, places

monetary demands on member countries for quotas that can only be

funded via each country's national deficit. This involves

the sale of government bonds to commercial banks, leading to

money creation by those banks. This source of revenue forms the

main fund of IMF monies available to developing nations.

Since the monetary demands on the IMF are constantly increasing,

due to rising demand for Third World loans, the quota demands by

the IMF have reached the point where (so-called) creditor

nations such as America and Britain are reluctant to undertake

yet more bond issues and further national debt to supply these

funds. So, in recent years the IMF has begun to

circumvent the restrictions of its overall quota. By

co-operating directly with commercial banks to organise more

substantial loans than it can fund from its own quota

resources, the IMF administers loan packages made up in part

from its own quotas and in part from commercial sources.

For example, of the $56 billion loan advanced under the IMF to

South Korea in the wake of the Asian crisis, only $20 billion

was contributed by the Fund; the remaining $36 billion was

arranged by direct co-operation with international commercial

banks, which created money for the purpose.

The total funds of the IMF were substantially increased and its

function and status as a money-creation agency clarified when,

in 1979, the IMF instituted Special Drawing Rights (SDRs). These

SDRs were created, and intended to serve, as an additional

international currency. Although these SDRs are credited to each

nations account with the IMF, if a nation borrows these SDRs

(defined in dollars) it must repay this amount, or pay interest

on the loan. Whilst SDRs are described as amounts credited to a

nation, no money or credit of any kind is put into nations

accounts. SDRs are actually a credit-facility just like a bank

overdraft if they are borrowed, they must be repaid. Thus,

the IMF is now creating and issuing money in the form of a

new international currency, created in parallel with debt, under

a system essentially the same as that of a bank... the IMF

reserve being the original pool of quota funds.

In summary, of the $2,200 billion currently outstanding as Third

World or developing country debt, the vast majority represents

money created by commercial banks in parallel with debt. In no

sense do the loans advanced by the World Bank and IMF constitute

monies owed to the creditor nations of the World Bank and

IMF. The World Bank co-operates directly with commercial

banks in the creation and supply of money in parallel with debt.

The IMF also negotiates directly with commercial banks to

arrange combined IMF/commercial loan packages.

As for those sums loaned by the IMF from the total quotas

supplied by member nations, these sums also do not constitute

monies owed to 'creditor' nations. The monies subscribed as

quotas were initially created by commercial banks through the

agency of national debts. Therefore both the contributing nation

and the borrowing Third World nation carry a

burden of debt associated with these sums. Both quotas and loans

are owed, ultimately, to commercial banks.

The Invalidity of Third World Debt, 1998, pp.14-17.

|

|

So...why is this a 'war on Islam'?

Islam does not charge interest on loans

the following is from Islam online...I think it is very illuminating.

A central bank such as the Federal Reserve in the US is the bank of the bankers. It is the lender of last resort. When no one else can lend money, the central bank can do so. How? It just writes down the money in the right account and "voila" the money is created out of nothing. Of course the borrower doesn't get it for nothing, but pays interest on this money created out of nothing. Treasury bonds play a key function in this because they are often bought by the Federal Reserve. Thus, giving the government an effectively unlimited supply of credit. If treasury bonds are sold in this way, they actually create extra liquidity not reduce it.

However, this is only one way in which money is created from nothing in the banking system and lent on interest. The other way involves what is called the fractional reserve system. This is where banks can take some money from your deposit account and without changing the amount in your account. They call the money thus taken as 'excess reserves', which then can be lent to someone else - of course with interest. Once the money is lent to that other person, inevitably the money returns to someone's deposit account where it can again be lent out. Depending on the fraction of money, held in deposit accounts required by the government, banks can lend, in this way, many multiples more cash than there is 'original money' ever placed into the banks. (There is no 'original money' anyway since it all originates in nothing but the instruction of a central banker.)

If all the money comes from creating debts in central banks and in other banks, where does the extra money come from to pay the interest? Well, there are 2 ways for getting this money. One is an ever-increasing volume of debt and the other is getting the bank to pay it by working in one way or another for the bank. In this way, every bit of money we earn comes from, not merely interest based loans, but loans from invented money. In this way, much of the world is enslaved to work for the banks, directly and indirectly. Once the loan is repaid, the money disappears magically the same way it was created.

Islam provides ways for financing to happen free from interest, which would bring about much greater justice and indeed "really produced" wealth in the world. Wealth comes from applying our minds and bodies to developing the natural world so as to produce benefits for people. It doesn't come from the endless speculations of systemically crisis ridden financial markets, with their booms and busts created from fictitious wealth. Interest, through its legal separation of investing money and the use of that money, detaches the financial markets from physical, human, and moral realities. Treasury bonds are a cornerstone of this system if not the very foundations. Without treasury bonds, the financial world would lose the most certain form, of interest based investment. Without the right to buy treasury bonds for invented money, the banking elite would lose one of their most profitable (literally) money making schemes.

see also

Banking Cartel is the Cause of Humanity's Woes

|

The case of riba:

Is there really a confusion?

There are many verses in the Qur’an having multiple interpretations but when it comes to riba (interest), Allah does not leave a single grey area when He clearly underlines that indulging in riba is like waging a war against Allah and His Prophet (PBUH). This leaves no doubt as to the banning of riba for all times to come. Therefore, even if Muslims are at a complete loss, there is no justification for not abolishing riba. Therefore it is clear, that whatever the circumstances, Muslims must not indulge in riba.

But the question is: what is riba? Unfortunately, this is the very question that has divided the Muslim scholars over the last few centuries into two main schools of thought, namely the Equivalence School and the Non-Equivalence School. According to the Equivalence School of thought, modern day interest and riba are co-equal and identical to each other and therefore modern day interest is banned in Islam. The proponents of Non-Equivalence School hold that modern day interest is distinct form the Quranic concept of Riba, which they believe refers only to the exploitative rates of interest, or usury. We can pretend to be confused, or be genuinely confused, about riba being modern day interest. The correct way is to really make an honest effort at finding out the truth. For this we have to first see the clear injunctions in the Qur’an about riba. Qur’an gives a very clear definition of Riba when, discussing riba it makes clear that in the event of giving a loan, Muslims can only get the repayment of the principal amount, and nothing more than that. If we just ponder over this ayah, we can straight away say, that whatever name you give to riba, whether you call it interest or usury, it is still riba and is haram. Another verse that could be used to define riba is when Allah says in the Quran that, He has clearly separated profit that we earn from trade, from riba, and that those who mix the two are like people who have been led astray by the satan. Thus riba is different from profit on trade. Now what is trade? Is this trade of goods, services or money?

To answer this question we must go back to our Prophet’s period and find out what was generally regarded as trade at that time. We find out that, in those times trade was generally referred to the trade in goods and services. The word trade was not used for transactions involving exchanging money with money. Obviously there were no stock exchanges at that time, nor were there banks. The only transactions that involved an exchange of money with money were where a creditor lent money to a borrower and later on got that money back, charging some amount over and above the principal. But this borrowing transaction was not referred to as trade in those times. Therefore, when Qur’an says that profit is allowed only on trade, that clearly means trade in goods and services.

One can earn profit on trade but not in borrowing transactions. Thus the interest earned in a borrowing transaction cannot be termed halal on the pretext that it is profit, just like profit on trade. Another verse that makes it clear that there is a difference between trading in goods and services and in borrowing, is when Allah specifically mentions a borrowing transaction at one place in the Qur’an. In this verse, Allah instructs a Muslim to give more time to his brother in religion when he is genuinely unable to return his money in time. Giving more time means waiting patiently, and obviously, does not mean charging any additional amount due to the delay. Allah goes to the extent of saying in the Holy Qur’an that if the borrower were facing some genuine difficulty in returning the money, it would be better if the creditor left the amount of principal altogether and treated it as a sadqa. Again, it becomes very obvious that Allah forbids us to charge anything over and above the principal. In fact, He wants us to be kind to the borrower, and not even ask for the principal amount in some genuine cases. There is another verse, which says that Allah promotes sadqa and eliminates riba. This shows that riba and sadqa are totally opposite transactions in their form and spirit. Sadqa is giving to others and sacrificing, riba is taking from the other person and forcing him to undergo suffering. Under this verse too, it becomes clearer that anything over and above the principle amount is forbidden.

If we refer to the verses pointed out in the above explanation, and try to understand their meaning deeply, it may become evident that the modern day bank interest, whatever is its rate, and by whatever name it is called, is riba. Now, the important point is not to mix the two: the banning of riba for all times by Allah, and our ability to follow this clear-cut injunction today because the whole economic system is based on riba. As mentioned above, we as Muslims are bound to follow the injunctions of Allah even if we are at a great loss. But we must remember, Allah does not want human beings in general, and Muslims in particular, to lose or be destroyed. He wants us to be successful both in this life and in the hereafter. Therefore, there is definitely some other way in which we can follow Allah’s injunctions and still be successful. We could find that way only if we do enough research and use the intellect and wisdom gifted to us by Allah to solve this problem. Allah Himself guides those who make genuine efforts in His way. - the muslim weekly.

|

is it me? or does it seem that if anyone wants

financial privacy, then they are

suspected of terrorism

|

Hawala

Mohammed El-Qorchi

How does this informal funds transfer system work, and should it be regulated?

Since the September 11, 2001, terrorist attacks on the United States, public interest in informal systems of transferring money around the world, particularly the hawala system, has increased. The reason is the hawala system's alleged role in financing illegal and terrorist activities, along with its traditional role of transferring money between individuals and families, often in different countries. Against this background, governments and international bodies have tried to develop a better understanding of these systems, assess their economic and regulatory implications, and design the most appropriate approach for dealing with them.

Informal funds transfer (IFT) systems are in use in many regions for transferring funds, both domestically and internationally. The hawala system is one of the IFT systems that exist under different names in various regions of the world. It is important, however, to distinguish the hawala system from the term hawala, which means "transfer" or "wire" in Arabic banking jargon. The hawala system refers to an informal channel for transferring funds from one location to another through service providers—known as hawaladars—regardless of the nature of the transaction and the countries involved. While hawala transactions are mostly initiated by emigrant workers living in a developed country, the hawala system can also be used to send funds from a developing country, even though the purpose of the funds transfer is usually different (see box).

|

How does the system work?

An initial transaction can be a remittance from a customer (CA) from country A, or a payment arising from some prior obligation, to another customer (CB) in country B. A hawaladar from country A (HA) receives funds in one currency from CA and, in return, gives CA a code for authentication purposes. He then instructs his country B correspondent (HB) to deliver an equivalent amount in the local currency to a designated beneficiary (CB), who needs to disclose the code to receive the funds. HA can be remunerated by charging a fee or through an exchange rate spread. After the remittance, HA has a liability to HB, and the settlement of their positions is made by various means, either financial or goods and services. Their positions can also be transferred to other intermediaries, who can assume and consolidate the initial positions and settle at wholesale or multilateral levels.

The settlement of the liability position of HA vis-�vis HB that was created by the initial transaction can be done through imports of goods or "reverse hawala." A reverse hawala transaction is often used for investment purposes or to cover travel, medical, or education expenses from a developing country. In a country subject to foreign exchange and capital controls, a customer (XB) interested in transferring funds abroad for, in this case, university tuition fees, provides local currency to HB and requests that the equivalent amount be made available to the customer's son (XA) in another country (A). Customers are not aware if the transaction they initiate is a hawala or a reverse hawala transaction. HB may use HA directly if funds are needed by XB in country A or indirectly by asking him to use another correspondent in another country, where funds are expected to be delivered. A reverse hawala transaction does not necessarily imply that the settlement transaction has to involve the same hawaladars; it could involve other hawaladars and be tied to a different transaction. Therefore, it can be simple or complex. Furthermore, the settlement can also take place through import transactions. For instance, HA would settle his debt by financing exports to country B, where HB could be the importer or an intermediary.

|

Why hawala developed

In earlier times, IFT systems were used for trade financing. They were created because of the dangers of traveling with gold and other forms of payment on routes beset with bandits. Local systems were widely used in China and other parts of East Asia and continue to be in use there. They go under various names—Fei-Ch'ien (China), Padala (Philippines), Hundi (India), Hui Kuan (Hong Kong), and Phei Kwan (Thailand). The hawala (or hundi) system now enjoys widespread use but is historically associated with South Asia and the Middle East. At present, its primary users are members of expatriate communities who migrated to Europe, the Persian Gulf region, and North America and send remittances to their relatives on the Indian subcontinent, East Asia, Africa, Eastern Europe, and elsewhere. These emigrant workers have reinvigorated the system's role and importance. While hawala is used for the legitimate transfer of funds, its anonymity and minimal documentation have also made it vulnerable to abuse by individuals and groups transferring funds to finance illegal activities.

Economic and cultural factors explain the attractiveness of the hawala system. It is less expensive, swifter, more reliable, more convenient, and less bureaucratic than the formal financial sector. Hawaldars charge fees or sometimes use the exchange rate spread to generate income. The fees charged by hawaladars on the transfer of funds are lower than those charged by banks and other remitting companies, thanks mainly to minimal overhead expenses and the absence of regulatory costs to the hawaladars, who often operate other small businesses. To encourage foreign exchange transfers through their system, hawaladars sometimes exempt expatriates from paying fees. In contrast, they reportedly charge higher fees to those who use the system to avoid exchange, capital, or administrative controls. These higher fees often cover all the expenses of the hawaladars.

The system is swifter than formal financial transfer systems partly because of the lack of bureaucracy and the simplicity of its operating mechanism; instructions are given to correspondents by phone, facsimile, or e-mail; and funds are often delivered door to door within 24 hours by a correspondent who has quick access to villages even in remote areas. The minimal documentation and accounting requirements, the simple management, and the lack of bureaucratic procedures help reduce the time needed for transfer operations.

In addition to economic factors, kinship, ethnic ties, and personal relations between hawaladars and expatriate workers make this system convenient and easy to use. The flexible hours and proximity of hawaladars are appreciated by expatriate communities. To accommodate their clients, hawaladars may instruct their counterparts to deliver funds to beneficiaries before expatriate workers make payments. Moreover, cultural considerations encourage expatriate workers to remit funds through the hawala system, and such considerations also apply to family members in the home country. Many expatriate communities are exclusively male, because wives and other family members remain in the home country, where family traditions prevail. These traditions may require family members, especially women, to maintain minimal contacts with the outside world. A trusted hawaladar, known in the village and aware of the social codes, would be an acceptable intermediary, protecting women from having direct dealings with banks and other agents. Thus, a system based on national, ethnic, and village solidarity depends more on absolute trust between the participants than on legal documents.

On the receiving side, repressive financial policies and inefficient banking institutions, which have often lacked interest in the remittance business, have contributed to the development of IFT systems. In addition to overly restrictive economic policies, unstable political situations have offered fertile ground for the development of the hawala and other informal systems. Most IFT systems have prospered in areas characterized by unsophisticated official systems and during times of instability. They continue to develop in regions where financial development has been slow or repressed. Overall, financial development tends to check the spread of informal fund transfer systems, even though they exist in financially mature countries as well.

Economic implications

Despite its informality, the hawala system has direct and indirect macroeconomic implications—for financial activity as well as for fiscal performance. One aspect is its potential impact on the monetary accounts of countries on either end of the hawala transaction. Because these transactions are not reflected in official statistics, the remittance of funds from one country to another is not recorded as an increase in the recipient country's foreign assets or in the remitting country's liabilities, unlike funds transferred through the formal sector. As a consequence, value changes hands, but broad money is unaltered. However, hawala transactions may affect the composition of broad money in a recipient country. In the remittance business, such transactions are conducted mainly in cash, even though hawaladars may use the banking system for other purposes. Individuals from developing countries who transfer funds abroad through the hawala system for investment or other purposes are usually members of wealthy groups. They supply local hawaladars with cash by making withdrawals from their bank accounts. As a consequence, hawala-type transactions tend to increase the amount of cash in circulation. Furthermore, IFT systems have fiscal implications for both remitting and receiving countries because no direct or indirect tax is paid on hawala transactions. The negative impact on government revenue applies equally to both legitimate and illegitimate activities that involve the hawala system.

Hawala transactions cannot be reliably quantified because records are virtually inaccessible, especially for statistical or balance of payments purposes. This holds true for both the remitting and, especially, the receiving sides of the transactions. Hawala transactions from developing countries are sometimes driven by capital flight motivations; they may also be driven by a desire to circumvent exchange control regulations and the like, leaving no traceable records. Nevertheless, the authorities of some countries have sporadically made estimates of hawala activity based on their expatriate populations and balance of payments data. In any case, all crude estimates should take into account both hawala and reverse hawala transactions (see box) as well as transactions driven by illicit activities. Although it would be impossible to provide a precise figure, the amounts involved in hawala transactions are likely to entail billions of dollars.

Difficulties for regulators

There is also a consensus that, in the wake of heightened international efforts to combat money laundering and terrorist financing, more should be done to keep an eye on IFT systems to avoid their misuse by illicit groups. Policymakers believe that the potential anonymity afforded by these systems presents risks of money laundering and terrorist financing that need to be addressed. Yet selecting the appropriate regulatory and supervisory response requires a realistic and practical assessment and an understanding of the specific country environment in which the IFT dealers operate.

Regulation of IFT systems in various jurisdictions will be a complex endeavor. The variety of legal systems and economic circumstances across countries make a uniform approach technically and legally impractical. In a number of countries, the hawala system is prohibited. Any attempt to regulate this system in these countries would, therefore, be at odds with existing laws and regulations and would be seen as legitimizing parallel foreign exchange operations and capital flight.

Where IFT regulations are conceivable, there is agreement that overregulation and coercive measures will not be effective because they might push IFT businesses, including legitimate ones, further underground. The purpose of any approach is not to eliminate these systems but to avoid their misuse. Against this background, policymakers tend to favor two options, which are already in force in some countries: registration or licensing of IFT systems.

While these measures could deter illegal activities, they will not, in isolation, succeed in reducing the attractiveness of the hawala system. As a matter of fact, as long as there are reasons for people to prefer such systems, they will continue to exist and even expand. If the formal banking sector intends to compete with the informal remittance business, it should focus on improving the quality of its service and reducing the fees charged. Therefore, a longer-term and sustained effort should be aimed at modernizing and liberalizing the formal financial sector, with a view to addressing its inefficiencies and weaknesses.

Mohammed El-Qorchi is a Senior Economist in the IMF's Monetary and Exchange Affairs Department.

|

that is, of course unless you bank offshore

George Soros is known as the wealthiest speculator of all time. His trading all took place in the Netherlands Antilles, where his earnings compounded tax free. If you think he has this advantage only because of his wealth read on.

Here is a list of Trend Followers with operations offshore:

John W. Henry Global Strategies Ltd. (A)

Sjo Global Fund Ltd. (B)

Eckhardt Futures LP

Mark J. Walsh Global LP

Chesapeake Fund Ltd.

Today, investing arenas are without borders. Investors may reside in Chicago or Kuala Lumpur, but geographic locales no longer need be a deterrent to investing globally. Offshore or non-US investments allow for more rigid controls on privacy. Privacy in an age of big brother is crucial to many investors. The US government along with numerous other over regulated industrialized societies have continued to threaten individual investor's privacy rights. Offshore funds are inherently private, a big selling point for global investors.

In examining offshore solutions one must be concerned with numerous issues. Services the trader or investor may need: fund organization, corporate management, domiciliary services, accounting and administration, shareholder services, banking and custodial issues, and computer data transmission.

Example Tax Haven Jurisdictions

Antigua

Bahamas

Belize

British Virgin Islands

Delaware

Gibraltar

Guernsey

Isle of Man

Jersey

Liberia

Mauritius

Nevis

Panama

Turks & Caicos Islands

If you wanted to, you could move or transfer some or all of your money out of your bank or credit union to anywhere in the world. This is entirely legal. US banks and the IRS disseminate negative propaganda dealing with offshore banking, making it seem unsafe or some type of criminal act. Why? Banks desire to keep money in their institutions to use for their own profitable purposes.

Most US banks themselves accept deposits from people overseas and often invest in foreign stocks and hold accounts with foreign banks. On the other hand the IRS wants to keep money in US banks where every dollar earned in interest can be taxed.

Another reason the US government has constructed US banking law in its present form is to prevent competition. The internet changes that forever. Now opening an account with an offshore bank is as simple as writing a formal letter to the institution and requesting information about their various services and the appropriate application forms. Most offshore centers never have to see you in person.

All offshore banks are regulated in one form or another, but the regulations are usually far less restrictive than US law. Less restrictive regulations abroad allow foreign banks more freedom in locating the best investments worldwide. Allowing them to pass on and share their profits with their customers. Additionally, the majority of the worlds largest and strongest banks are non-US banks.

- excerpted from turtletraders guide to offshore banking

|

"Dirty Money" is the Foundation of U.S. Growth and Empire

Size and Scope of Money Laundering by U.S. Banks From La Journada [Mexico], 2005.01.19

by James Petras - Professor of Sociology, Binghamton University

There is a consensus among U.S. Congressional Investigators, former bankers and international banking experts that U.S. and European banks launder between $500 billion and $1 trillion of dirty money each year, half of which is laundered by U.S. banks alone. As Senator Carl Levin summarizes the record: "Estimates are that $500 billion to $1 trillion of international criminal proceeds

are moved internationally and deposited into bank accounts annually. It is estimated that half of that money comes to the United States".

Over a decade then, between $2.5 and $5 trillion criminal proceeds have been laundered by U.S. banks and circulated in the U.S. financial circuits. Senator Levin's statement however, only covers criminal proceeds, according to U.S. laws. It does not include illegal transfers and capital flows from corrupt political leaders, or tax evasion by overseas businesses. A leading U.S. scholar who is an expert on international finance associated with the prestigious Brookings Institute estimates "the flow of corrupt money out of developing (Third World) and transitional (ex-Communist) economies into Western coffers at $20 to $40 billion a year and the flow stemming from mis-priced trade at $80 billion a year or more. My lowest estimate is $100 billion per year by these two means by which we facilitated a trillion dollars in the decade, at least half to the United States. Including the other elements of illegal flight capital would produce much higher figures. The Brookings expert also did not include illegal shifts of real estate and securities titles, wire fraud, etc.

In other words, an incomplete figure of dirty money (laundered criminal and corrupt money) flowing into U.S. coffers during the 1990s amounted to $3-$5.5 trillion. This is not the complete picture but it gives us a basis to estimate the significance of the "dirty money factor" in evaluating the U.S. economy. In the first place, it is clear that the combined laundered and dirty money flows cover part of the U.S. deficit in its balance of merchandise trade which ranges in the hundreds of billions annually. As it stands, the U.S. trade deficit is close to $300 billion. Without the "dirty money" the U.S. economy external accounts would be totally unsustainable, living standards would plummet, the dollar would weaken, the available investment and loan capital would shrink and Washington would not be able to sustain its global empire. And the importance of laundered money is forecast to increase. Former private banker Antonio Geraldi, in testimony before the Senate Subcommittee projects significant growth in U.S. bank laundering. "The forecasters also predict the amounts laundered in the trillions of dollars and growing disproportionately to legitimate funds." The $500 billion of criminal and dirty money flowing into and through the major U.S. banks far exceeds the net revenues of all the IT companies in the U.S., not to speak of their profits. These yearly inflows surpass all the net transfers by the major U.S. oil producers, military industries and airplane manufacturers. The biggest U.S. banks, particularly Citibank, derive a high percentage of their banking profits from serving these criminal and dirty money accounts. The big U.S. banks and key institutions sustain U.S. global power via their money laundering and managing of illegally obtained overseas funds.

U.S. Banks and The Dirty Money Empire

Washington and the mass media have portrayed the U.S. as being in the forefront of the struggle against narco trafficking, drug laundering and political corruption: the image is of clean white hands fighting dirty money. The truth is exactly the opposite. U.S. banks have developed a highly elaborate set of policies for transferring illicit funds to the U.S., investing those funds in legitimate businesses or U.S. government bonds and legitimating them. The U.S. Congress has held numerous hearings, provided detailed exposés of the illicit practices of the banks, passed several laws and called for stiffer enforcement by any number of public regulators and private bankers. Yet the biggest banks continue their practices, the sum of dirty money grows exponentially, because both the State and the banks have neither the will nor the interest to put an end to the practices that provide high profits and buttress an otherwise fragile empire.

First thing to note about the money laundering business, whether criminal or corrupt, is that it is carried out by the most important banks in the USA. Secondly, the practices of bank officials involved in money laundering have the backing and encouragement of the highest levels of the banking institutions - these are not isolated cases by loose cannons. This is clear in the case of Citibank's laundering of Raul Salinas (brother of Mexico's ex-President) $200 million account. When Salinas was arrested and his large scale theft of government funds was exposed, his private bank manager at Citibank, Amy Elliott told her colleagues that "this goes in the very, very top of the corporation, this was known...on the very top. We are little pawns in this whole thing" (p.35).

Citibank, the biggest money launderer, is the biggest bank in the U.S., with 180,000 employees world-wide operating in 100 countries, with $700 billion in known assets and over $100 billion in client assets in private bank (secret accounts) operating private banking offices in 30 countries, which is the largest global presence of any U.S. private bank. It is important to clarify what is meant by "private bank."

Private Banking is a sector of a bank which caters to extremely wealthy clients ($1 million deposits and up). The big banks charge customers a fee for managing their assets and for providing the specialized services of the private banks. Private Bank services go beyond the routine banking services and include investment guidance, estate planning, tax assistance, off-shore accounts, and complicated schemes designed to secure the confidentiality of financial transactions. The attractiveness of the "Private Banks" (PB) for money laundering is that they sell secrecy to the dirty money clients. There are two methods that big Banks use to launder money: via private banks and via correspondent banking. PB routinely use code names for accounts, concentration accounts (concentration accounts co-mingles bank funds with client funds which cut off paper trails for billions of dollars of wire transfers) that disguise the movement of client funds, and offshore private investment corporations (PIC) located in countries with strict secrecy laws (Cayman Island, Bahamas, etc.)

For example, in the case of Raul Salinas, PB personnel at Citibank helped Salinas transfer $90 to $100 million out of Mexico in a manner that effectively disguised the funds' sources and destination thus breaking the funds' paper trail. In routine fashion, Citibank set up a dummy offshore corporation, provided Salinas with a secret code name, provided an alias for a third party intermediary who deposited the money in a Citibank account in Mexico and transferred the money in a concentration account to New York where it was then moved to Switzerland and London.

The PICs are designed by the big banks for the purpose of holding and hiding a person's assets. The nominal officers, trustees and shareholder of these shell corporations are themselves shell corporations controlled by the PB. The PIC then becomes the holder of the various bank and investment accounts and the ownership of the private bank clients is buried in the records of so-called jurisdiction such as the Cayman Islands. Private bankers of the big banks like Citibank keep pre-packaged PICs on the shelf awaiting activation when a private bank client wants one. The system works like Russian Matryoshka dolls, shells within shells within shells, which in the end can be impenetrable to a legal process.

The complicity of the state in big bank money laundering is evident when one reviews the historic record. Big bank money laundering has been investigated, audited, criticized and subject to legislation; the banks have written procedures to comply. Yet banks like Citibank and the other big ten banks ignore the procedures and laws and the government ignores the non-compliance.

Over the last 20 years, big bank laundering of criminal funds and looted funds has increased geometrically, dwarfing in size and rates of profit the activities in the formal economy. Estimates by experts place the rate of return in the PB market between 20-25% annually. Congressional investigations revealed that Citibank provided "services" for 4 political swindlers moving $380 million: Raul Salinas - $80-$100 million, Asif Ali Zardari (husband of former Prime Minister of Pakistan) in excess of $40 million, El Hadj Omar Bongo (dictator of Gabon since 1967) in excess of $130 million, the Abacha sons of General Abacha ex-dictator of Nigeria - in excess of $110 million. In all cases Citibank violated all of its own procedures and government guidelines: there was no client profile (review of client background), determination of the source of the funds, nor of any violations of country laws from which the money accrued. On the contrary, the bank facilitated the outflow in its prepackaged format: shell corporations were established, code names were provided, funds were moved through concentration accounts, the funds were invested in legitimate businesses or in U.S. bonds, etc. In none of these cases - or thousands of others - was due diligence practiced by the banks (under due diligence a private bank is obligated by law to take steps to ensure that it does not facilitate money laundering). In none of these cases were the top banking officials brought to court and tried. Even after arrest of their clients, Citibank continued to provide services, including the movement of funds to secret accounts and the provision of loans.

Correspondent Banks: The Second Track

The second and related route which the big banks use to launder hundreds of billions of dirty money is through "correspondent banking" (CB). CB is the provision of banking services by one bank to another bank. It is a highly profitable and significant sector of big banking. It enables overseas banks to conduct business and provide services for their customers - including drug dealers and others engaged in criminal activity - in jurisdictions like the U.S. where the banks have no physical presence. A bank that is licensed in a foreign country and has no office in the United States for its customers attracts and retains wealthy criminal clients interested in laundering money in the U.S. Instead of exposing itself to U.S. controls and incurring the high costs of locating in the U.S., the bank will open a correspondent account with an existing U.S. bank. By establishing such a relationship, the foreign bank (called a respondent) and through it, its criminal customers, receive many or all of the services offered by the U.S. big banks called the correspondent.

Today, all the big U.S. banks have established multiple correspondent relationships throughout the world so they may engage in international financial transactions for themselves and their clients in places where they do have a physical presence. Many of the largest U.S. and European banks located in the financial centers of the world serve as correspondents for thousands of other banks. Most of the offshore banks laundering billions for criminal clients have accounts in the U.S. All the big banks specializing in international fund transfer are called money center banks, some of the biggest process up to $1 trillion in wire transfers a day. For the billionaire criminals an important feature of correspondent relationships is that they provide access to international transfer systems - that facilitate the rapid transfer of funds across international boundaries and within countries. The most recent estimates (1998) are that 60 offshore jurisdictions around the world licensed about 4,000 offshore banks which control approximately $5 trillion in assets.

One of the major sources of impoverishment and crises in Africa, Asia, Latin America, Russia and the other countries of the ex-U.S.S.R. and Eastern Europe, is the pillage of the economy and the hundreds of billions of dollars which are transferred out of the country via the corresponding banking system and the Private Banking system linked to the biggest banks in the U.S. and Europe. Russia alone has seen over $200 billion illegally transferred in the course of the 1990s. The massive shift of capital from these countries to the U.S. and European banks has generated mass impoverishment and economic instability and crises. This in turn has created increased vulnerability to pressure from the IMF and World Bank to liberalize their banking and financial systems leading to further flight and deregulation which spawns greater corruption and overseas transfers via private banks as the Senate reports demonstrate.

The increasing polarization of the world is embedded in this organized system of criminal and corrupt financial transactions. While speculation and foreign debt payments play a role in undermining living standards in the crisis regions, the multi-trillion dollar money laundering and bank servicing of corrupt officials is a much more significant factor, sustaining Western prosperity, U.S. empire building and financial stability. The scale, scope and time frame of transfers and money laundering, the centrality of the biggest banking enterprises and the complicity of the governments, strongly suggests that the dynamics of growth and stagnation, empire and re-colonization are intimately related to a new form of capitalism built around pillage, criminality, corruption and complicity.

-- James Petras is a Professor of Sociology at Binghamton University in Binghamton, New York. He is the author of 57 books. His latest is "Globalization Unmasked: Imperialism in the New Millennium." - via indymedia.org.uk

|

|

Muslim brotherhood - Perversion of Islam for BIG business - Nazi collaborators

Discussing the diaspora of the Muslim Brotherhood following its expulsion from Egypt, the program discusses the establishment of Munich as its primary base of operations.

'Why Munich, why Germany?' I asked Rifaat Said. 'Because there, one finds old complicities that go back to the late 1930's, when the Muslim Brothers collaborated with the agents of Nazi Germany. . . By soaking up the savings of these Muslim workers, Yussef Nada, like Said Ramadan, took advantage of an extremely favorable context and used it as a springboard for the Muslim Brothers' economic activities.'

Nada himself (the head of the Brotherhood's Bank Al Taqwa) is alleged to have been an agent of the Abwehr, the military intelligence service of the Third Reich. (See FTR#416.) "But Yussef Nada is even better-known to the Egyptian [intelligence] services, who have evidence of his membership in the armed branch of the fraternity of the Muslim Brothers in the 1940's. At that time, according to the same sources, he was working for the Abwehr under Admiral Canaris and took part in a plot against King Farouk. This was not the first time that the path of the Muslim Brothers crossed that of the servants of the Third Reich."

"Muhammad Said al-Ashmawy continued: 'All my research always brings me back to the same point: at the beginning of this process of the perversion of Islam are the Muslim Brothers, an extreme Right cult.'. . . An extreme Right cult? 'The history of the Muslim Brothers is infused and fascinated by fascistic ideology,' Said al-Ashmawy adds. 'Their doctrines, their total (if not totalitarian) way of life, takes as a starting point the same obsession with a perfect city on earth, in conformity with the celestial city whose organization and distribution of powers they can discern through the lens of their fantastical reading of the Koran.' This 'Fascistic affiliation' would crop up in the analyses of several of our interlocutors, in particular that of the journalist Eric Rouleau, who is a specialist in the Middle East, former French ambassador to Tunisia and Turkey."

Al Taqwa - A financial system built to launder & cover it's ass!

...this bank, Al Taqwa, is suspected by the FBI, this shortly after the 11th of September, to have taken part in the financing of Bin Laden. It [Al Taqwa] is reproduced on the black list of the Americans. However, this kind of Islamic bank is quasi-impenetrable. It does not have the right to make interest, it thus makes assemblages of risk capital.

Translation: it invests in concrete operations, financing of NGO, etc. In fact, multi-stage financial arrangements feed a myriad of charitable organizations. It is what the specialists call bleaching back [laundering] it is a zigzag, a labyrinth in which the investigators lose themselves, inevitably. When one examines the financial exercises of these establishments, a whole fringe of their activities is registered under the heading of zakat, the religious tax, the obligation of charity, a truly forbidden zone. However one knows that the zakat is used to finance offshore companies, protected perfectly by the same bank secrecy, and also the Islamic NGO's, which are completely unverifiable and uncontrolled. Thus, since November 2001, bank Al Taqwa changed names but Yussef Nada, the friend of Said Ramadan, continues its activities. The investigation does nothing but create publicity."

From David Emory's Compendium on the Muslim Brotherhood

|

Do these two systems seek to work work in tandem?

one is built on invention of interest,

which then channels huge invented profits.

While another seemingly a system built on a labyrithian process,

which conveniently uses religion as a cover.

from the Rev. Moon to Christian Dominionists to Islamofascist theocracy.

The aim for these systems is the enslavement the entire world population

These power nazis will go to any lengths to bring an uncompliant system to it's knees.

|

The Fellowship - theocratic synarchy?

"The Fellowship believes that ANYTHING is permitted in order to bring about a 1000-yr Kingdom of Christ on Earth, and that includes stealing elections and even murder."

Madsen: End of Year Update on Investigation

|

|

|

Someone is getting very jumpy!

Investigative reporter Gary Webb found dead...suicided?

Gary Webb, an investigative reporter who wrote a widely criticized series linking the CIA to the explosion of crack cocaine in Los Angeles, was found dead in his Sacramento-area home Friday. He apparently killed himself, authorities said. Webb had suffered a gunshot wound to the head, according to the Sacramento County coroner's office. He was 49.

|

|

His 1996 San Jose Mercury News series contended that Nicaraguan drug traffickers had sold tons of crack cocaine from Colombian cartels in Los Angeles' black neighborhoods and then funneled millions in profits back to the CIA-supported Nicaraguan Contras. Three months after the series was published, the Los Angeles County Sheriff's Department said it conducted an exhaustive investigation but found no evidence of a connection between the CIA and Southern California drug traffickers. -

GARY WEBB: THE STORY YOU WON'T READ

Gary Webb was investigating ACS [computer systems as pert of vote fraud] and contract fraud in CA when he committed suicide on Dec. 10.

- Wayne Madsen also see: 2004 election fraud

Gary Webbs Dark Alliance site

see also:

Neo christian godhead

Bush: The fellowship or the ring?

|

whoops! |

UN unveils plan to release untapped wealth of...$7 trillion

(and solve the world's problems at a stroke)

By Philip Thornton, Economics Correspondent Published: 30 January 2006

The most potent threats to life on earth - global warming, health pandemics, poverty and armed conflict - could be ended by moves that would unlock $7 trillion - $7,000,000,000,000 (£3.9trn) - of previously untapped wealth, the United Nations claims today.

The price? An admission that the nation-state is an old-fashioned concept that has no role to play in a modern globalised world where financial markets have to be harnessed rather than simply condemned.

In a groundbreaking move, the UN Development Programme (UNDP) has drawn up a visionary proposal that has been endorsed by a range of figures including Gordon Brown, the Chancellor of the Exchequer, and Joseph Stiglitz, the Nobel Laureate. It says an unprecedented outbreak of co-operation between countries, applied through six specific financial tools, would slice through the Gordian knot of problems that have bedevilled the world for most of the last century.

If its recommendations are accepted - and the authors acknowledge this could take years or even decades - it could finally force countries to face up to the fact that their public finance and growth figures conceal the vast damage their economies do to the environment.

At the heart of the proposal, unveiled at a gathering of world business leaders at the Swiss ski resort of Davos, is a push to get countries to account for the cost of failed policies, and use the money saved "up front" to avert crises before they hit. Top of the list is a challenge to the United States to join an international pollution permit trading system which, the UN claims, could deliver $3.64trn of global wealth.

Inge Kaul, a special adviser at the UNDP, said: "The way we run our economies today is vastly expensive and inefficient because we don't manage risk well and we don't prevent crises." She downplayed concerns over up-front costs and interest payments for the new-fangled financial devices. "The gains in terms of development would outweigh those costs. Money is wasted because we dribble aid, and the costs of not solving the problems are much, much higher than what we would have to pay for getting the financial markets to lend the money."

The UNDP is determined to ensure globalisation, which has generated vast wealth for multinational companies, benefits the poorest in society.

It urges politicians to embrace some groundbreaking schemes put in place in the past 12 months to tackle global warning, poverty and disease, based on working with the global markets to share out the risk.

These include a pilot international finance facility (IFF) to "front load" $4bn of cash for vaccines by borrowing money against pledges of future government aid.

The scheme, which is backed by the UK, France, Italy, Spain, Sweden and the Bill and Melinda Gates Foundation, was born out of a proposal by Gordon Brown for a larger scheme to double the total aid budget to $100bn a year.

In an endorsement of the report, Mr Brown said: "This shows how we can equip people and countries for a new global economy that combined greater prosperity and fairness both within and across nations."

The UNDP says rich countries should build on this and go further. It proposes six schemes to harness the power of the markets:

* Reducing greenhouse gas emissions through pollution permit trading; net gain $3.64trn.

* Cutting poor countries' borrowing costs by securing the debts against the income from stable parts of their economies; net gain $2.90trn.

* Reducing government debt costs by linking payments to the country's economic output; net gain $600bn.

* An enlarged version of the vaccine scheme; net gain (including benefits of lower mortality) $47bn.

* Using the vast flow of money from migrants back to their home country to guarantee; net gain $31bn.

* Aid agencies underwriting loans to market investors to lower interest rates; net gain $22bn.

Professor Stiglitz, the former chief economist of the World Bank and a staunch critic of the way globalisation harms the poor, said: "Globalisation has meant the closer integration of countries, and that in turn has meant a greater need for collective action. "One of the most important areas of failure is the environment. Without government intervention, firms and households have no incentive to limit their pollution." He said a global public finance system would force countries to acknowledge the external damage their policies had, "the most important being global climate change".

Solving the environmental crisis tops the UN's $7trn wish-list. It calls for an international market to trade pollution permits that would encourage rich countries to cut pollution and hit their targets under the Kyoto protocol. But - and the UN admits it is a big "but" - the US would have to sign up to Kyoto and carbon trading to achieve the $3.64trn that it believes the system would deliver over time.

"We are dealing with a global problem as pollution can only be dealt with internationally," Ms Kaul said. Richard Sandor, the head of the Chicago Climate Exchange, added: "Many encouraging signs are emerging. When the business case is clear, private entrepreneurs step forward."

But, the proposal is unlikely to get support from some green groups who believe that action to curb consumption, rather than market incentives, are the way to reduce carbon emissions.

Andrew Simms, director of the New Economics Foundation, said it left unanswered questions over how these markets would be managed and how the benefits and costs would be distributed. "We have nothing against markets so it would be missing the point to get into a pro- or anti-market stance. The point is how you distribute the benefits." He said the Nineties, the zenith decade for globalisation, had seen just 60 cents out of every $100 worth of growth reach the poorest in society, compared with the $2.20 in the Eighties. He said a pollution trading regime had the potential to deliver "enormous" benefits to poor countries, but said the UN report failed to show a detailed plan. "Our view is that you have to cap pollution, allocate permits and then you can trade. But it depends on how it is set up. Because you are dealing with a global commons of the atmosphere, the danger is that you could be effectively dealing in stolen goods." He said a system set up now to trade in pollution permits could end up permanently depriving poor countries that joined the system further down the road.

International problems - and solutions

PANDEMIC DISEASES

Millions of people across the developing world have died from malaria, tuberculosis and HIV/Aids, as well as from other pandemics. Vaccines needed to avert them require much-needed investment.

SOLUTION: An advance commitment by rich countries to buy $3bn (£1.7bn) worth of vaccines would be enough to encourage pharmaceutical giants to invest in finding medicines that would eliminate these pandemics.

SAVING: $600bn

ALTERNATIVE SOLUTION: Vaccines are needed but more should be done in the meantime. Extra aid is needed for simple tools such as mosquito nets that would curb spread of malaria.

PARIAH STATES

Big business and global money ignore countries where they see the risk of conflict outweighing their potential profit margins.

SOLUTION: Guarantees by international organisations such as the International Monetary Fund to lower the cost of borrowing for poor nations by underwriting investors' loans to conflict-torn states.

SAVING: $22bn

ALTERNATIVE SOLUTION: Sometimes large volumes of cash are needed and this is one. Live8 showed there was huge support among taxpayers for higher aid to countries in distress.

Hitting a commitment made in the 1960s of 0.7 per cent of GDP would unlock $140bn a year.

NATIONAL BANKRUPTCY

Once great nations such as Brazil and Argentina were reduced to the status of beggars after poor economic policy combined with debts with national and international lenders.

SOLUTION: A system to enable countries to take loans linked to their average economic growth rate to ensure that they do not have to cut public spending to raise the money to borrow needed funds during the hard times.

SAVING: $600bn

ALTERNATIVE SOLUTION: A system to allow countries to seek protection from their creditors in the same way that US companies can take so-called Chapter 11 bankruptcy.

SPECULATIVE INVESTORS

Poor countries suffer most from swings in investment tastes by the big global investors that means money can leave as soon as it arrives.

SOLUTION: Enable countries to buy "insurance policies" against big swings in growth that would ensure that they did not have to cut public spending every time. In 1997 it wreaked havoc across South-east Asia.

SAVING: $2,900bn

ALTERNATIVE SOLUTION: Curb speculative investment by imposing a tax on foreign exchange transactions aimed at destabilising a currency. It could directly raise funds for development while preventing the worst excesses of the markets.

GLOBAL WARMING

Scientists believe human activity has led to climate change and disappearing Arctic ice. The world's poor also have to live with lethal storms and floods.

UN SOLUTION: A system of international trading in permits to allow pollution that would encourage countries to cut their emission of greenhouse gases so they can sell their "right to pollute" to other states. UNDP says it is more effective than just setting targets.

SAVING: $3,620bn

ALTERNATIVE SOLUTION: An international approach is needed but one that prevents people from causing harm by setting pollution targets rather than trying to bribe them not to. Also agree global airline tax.

BRAIN DRAIN

Millions of skilled workers leave their home countries every year in search of a better life in the West. In some states nine out 10 professionals have left.

SOLUTION: Enable countries to borrow on the open markets against the money workers send home. The capital would be used to invest in the country to build infrastructure that would discourage people from leaving.

SAVING: $31bn

ALTERNATIVE SOLUTION: An international code of ethical guidelines overseen by bodies such as the World Health Organisation (for doctors and nurses) to monitor the harm that migration of professionals causes.

UK independent

|